Having something to look forward to in the future is always an exciting feeling – whether it’s a new car, holiday, or house. But for many people, saving up for big-ticket items can often seem impossible and might even require a small loan to make it happen. That’s why it’s important you have a savings plan to reach your short term savings goals and long term saving goals.

To help you out, Swoosh has compiled a few top tips to get you started on your saving journey! Here is our six-step plan to help you start saving for your short and long term goals today. But first, let’s cover what some of those short and long term goals might be.

Overview

- Assess your current position

- Set your long and short term savings goals

- Pay off debt as soon as possible

- Split your savings

- Automate your savings

- Stick to the plan

What is short term saving?

It’s when you put money aside to meet a short term savings goal, typically within 5 years.

What are examples of short term savings goals?

You could save for:

- Holiday

- Wedding

- Engagement ring

- Minor repairs and home improvements

- New technology (laptop, television etc.)

What is a long term savings plan?

A long term savings plan helps you set aside enough money over a longer period of time to cover a big cost. You may be saving for a particular big expense, or so you have enough funds on hand to take advantage of a sudden opportunity.

What are long term savings goal examples?

You could save for:

- Retirement

- House

- New car

- Extended period of travel

- Unexpected medical emergency

How to plan short & long-term savings goals

Step 1 – Assess your current position

Start by writing down a full list of your income and expenses.

Income

This includes your EXPECTED sources of income. Don’t include things like lottery winnings, no matter how confident you are! Income could come from the following sources:

- Wages

- Dividends from interest

- Royalties

- Rental income

- Earnings from a business

Expenses

Monthly or fortnightly

- Rent/mortgage

- Groceries

- Fuel

- Unsecured or secured loan repayments

- Subscriptions (e.g. Netflix, gym)

- Entertainment (e.g. nights out)

Annual or quarterly

- Utility bills

- Insurance

- Vehicle registration and maintenance

Top tip: Breaking quarterly expenses into a weekly cost can help you put aside money to pay them when they are due.

Step 2 – Set your long and short term savings goals

Now that you know where you are financially, you can figure out where you want to go. Your goals may include paying down debt, saving for the future, building an emergency fund or saving for a specific item. Once you set your long and short term savings goals you can create a budget that will help you systematically work towards them.

Top tip: Prioritise your expenses. Fixed expenses such as rent and food come first, then savings/debt repayments, then variable expenses such as entertainment.

Step 3 – Pay off debt as soon as possible

Hands-down the easiest way to save money is to pay down your debt as quickly as possible. You should focus first on high-interest debt such as credit cards and small personal loans. Although there might be a temptation to save money at the same time, by focusing all of your money into paying debts first, you will save money in the long run.

Money owed on things like high-interest credit cards can amass very quickly, and the interest you are paying is likely to be more than you will make from the stock market or high-interest bank accounts. Over time, this increasing debt has the power to eat back into your savings, or see you spiral into greater debt.

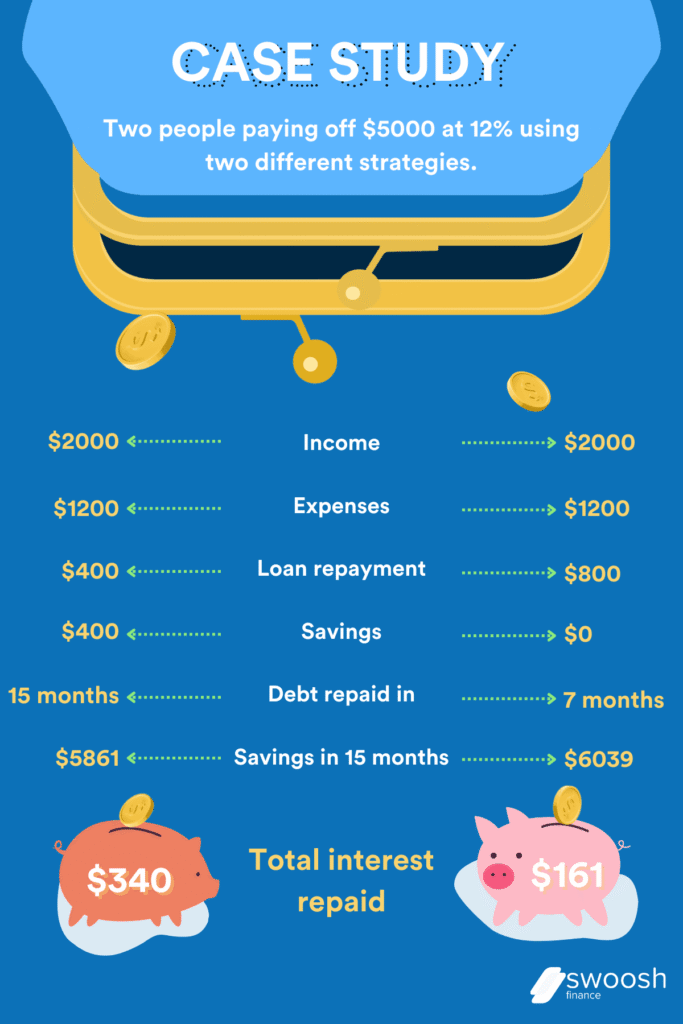

To illustrate the point, let’s do a comparison. In this case study, we’ll look at 2 people repaying a $5000 debt at 12%pa. Person A repays the minimum $400 per month and saves $400 per month. Person B pays $800 per month until the loan is paid and then saves once it is paid off.

As you can see Person B is ahead by almost $200 by the end. Both people have the same income and expenses, the only change is how they are paying off their debt.

This isn’t to say that paying off debt should always take precedent. Putting away money for an emergency fund is a great idea – just put the largest chunk of your money (after expenses) towards paying off high interest debt. You might also want to consider getting a debt consolidation loan, which can consolidate all your debt and reduce your interest, fees, and monthly payments.

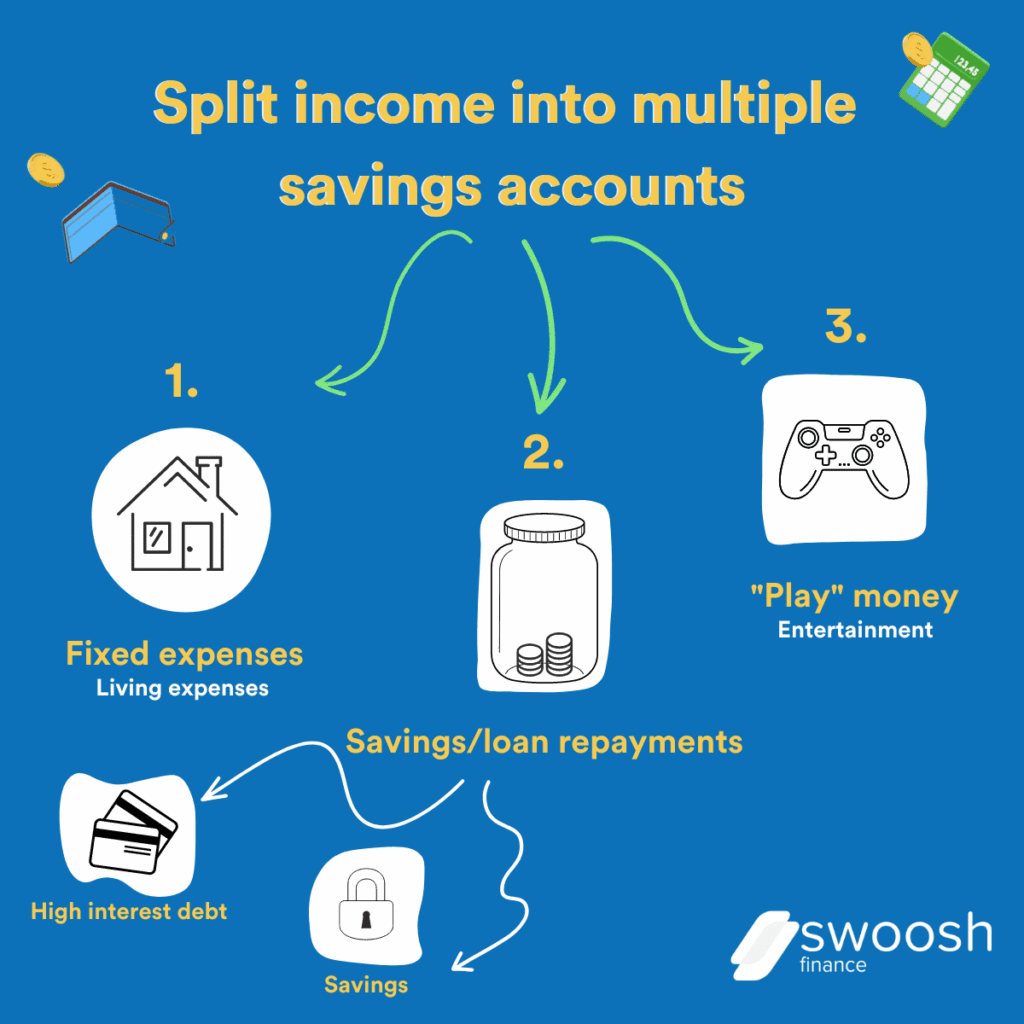

Step 4 – Split your savings

Now that you have set your short and long term savings goals, paid off your debt, and are saving money, you are ready for our next tip!

You should always have two or more separate accounts for savings. One for short-term savings goals like a holiday or other luxury items, and another for long-term savings goals. The idea is not to touch the long-term savings until you have reached your goal. This may be buying a house, saving for retirement or an investment opportunity. Either way, the long-term savings account is not for that new jacket or fishing rod.

You may also choose to have one or two other savings accounts. One can be used for necessities such as utility bills and car registration or other essentials that pop up on a not-so-regular basis, like vet bills. The other one can be for things you want to splurge on but don’t need – like a holiday or a new toy.

By structuring your savings this way you fulfil three basic financial needs – security for the future, having money for bills when you need it, and being able to treat yourself.

Step 5 – Automate your savings

This one is simple. By prioritising your savings you can change your habits and foster a savings mentality.

Setting up withdrawals to automatically come out of your account helps you save in two ways. Firstly, money is taken out of your account and placed into a high interest savings account to accrue interest. More money in these types of accounts means more interest.

Secondly, you get a lifestyle change. Because the money is automatically transferred out, you’ll actually be spending less money on other non-essential things each month. This ultimately leads to new spending habits that can last long into the future.

Step 6 – Stick to the plan!

This is the hardest and most important part! The key to meeting your long and short term savings goals is to leave some wiggle room in your budget each week. After all, life is for living, so make sure you allocate a little bit of money each week to treat yourself.

This blog post has some great tips on how to curb impulse spending.

BONUS TIP: Get a piggy bank for loose change

Although it may seem like an outdated or childish thing to do, having a piggy bank in your home is a very underrated way to save money.

Every time you might have loose change in your wallet, it’s a great idea to drop it into your piggy bank (you don’t have to buy an actual pig-shaped moneybox, any container will do!). This can be a highly effective saving method because the loose change is rarely missed. And it has the power to add up significantly over time – even just $2 a day can add up to over $700 a year.

Once you think your piggy bank starts getting heavy from all the change you’ve been regularly depositing, take it into your bank branch and put it directly into your savings.

Almost reached your short or long term savings goal?

If you’ve been saving for a while and are just within reach of your short term or long term savings goal, Swoosh can offer the help you need. We know you have the power to save, which is why our fixed term loans are perfect for people who need that little bit extra to play around with. Scheduled repayments make things even easier – contact us today to learn more about our easy online loans.