In Australia, we’re very fortunate to have access to a public healthcare system, known as Medicare. But unfortunately, Medicare doesn’t cover everything. So is it worth investing in private health insurance to take care of those out-of-pocket expenses? Or should you consider other options, like an emergency loan, if the need ever arises? It all depends on your individual circumstances. So to help you, we’ve broken down the advantages and disadvantages of Medicare vs private health insurance. Read on to learn more!

Overview:

- What is Medicare?

- What is private health insurance?

- How do Medicare and private health insurance affect your taxes?

- What is the difference between Medicare & private health insurance?

- Medicare vs private health insurance: pros & cons

- Do you need Medicare if you have private health insurance?

- Is Medicare or private insurance better?

- Medicare vs private health insurance FAQs

What is Medicare?

Medicare is a universal health insurance scheme available to Australian citizens and permanent residents. It covers or subsidises the cost of hospital services, medical services, tests, imaging, and scans. For example, if your GP bulk bills, Medicare covers the full cost of your visit. If they don’t, you’ll pay upfront and then claim some or all of the cost back through a Medicare rebate.

Medicare’s free or subsidised costs mean Australia has some of the most affordable and accessible medical services in the world (excluding dental).

And Medicare almost didn’t happen! In 1976, the new government dismantled Medibank (Medicare’s predecessor), leading to Australia’s first (and so far only) nationwide strike. It’s because of this national action that we all get to enjoy free universal healthcare today.

What does Medicare cover?

The following is covered by Medicare:

- Part or all of the cost of seeing a GP or specialist

- Most prescription medicines

- Emergency hospital care

- Most surgeries

- Treatment and accommodation in public hospitals

- Eye tests

- Every 3 years for under-65s

- Every year for over-65s

- Pathology tests for screening, diagnosis, or monitoring

You may have to pay a portion of the cost out-of-pocket (or with private health insurance) if your doctor or specialist charges more than the Medical Benefits Schedule (MBS) fee.

Note that as a public patient in a public hospital, you’ll be treated by hospital-appointed doctors and subject to waitlists for non-emergency treatment.

Through Medicare, you can also get a subsidised or covered care plan for the following:

- Mental health treatment

- Eating disorder care

- GP Chronic condition management

- Complex neurodevelopmental conditions and eligible disabilities

These plans are usually limited by a specified number of sessions or services.

What does Medicare not cover?

When considering Medicare vs private health insurance, you must consider what Medicare doesn’t cover, which includes:

- Dental

- Ambulance services*

- Glasses/contact lenses

- Hearing aids

- Elective surgery

- Cosmetic surgery

- Non-MBS and private health system services

This is where private health insurance can fill the gaps and give you more choice over treatment.

*If you are a resident of Queensland or Tasmania, you don’t have to pay ambulance costs as it’s covered by your taxes.

What is private health insurance?

As the name suggests, having private health care allows you to access the private health system. You can purchase private health insurance from a registered health insurer, in which you will pay regular premiums to maintain your cover.

What does private health insurance cover in Australia?

There are many different levels of cover to choose from, and it can include things like:

- Hospital cover

- Extras cover (such as dental, physiotherapy or optical)

- Ambulance cover

Most insurers offer a Medical Gap Scheme (also called Gap Cover), which can reduce or remove the “gap” between what Medicare pays and what your doctor charges in hospital.

However, this only applies to certain doctors and treatments.

What does private health insurance not cover?

There are some things that are not covered by private health that are covered by Medicare, including:

- GP visits and some specialists

- Both public and private hospital emergency department visits

- Outpatient medical services that are covered by Medicare

- Most of the cost of out-of-hospital specialist consultations

- Outpatient diagnostic imaging and tests e.g. x-rays and blood tests

- Some natural therapies

How does private health insurance work?

It’s important to note that private health insurance doesn’t mean you are fully covered for any health issue. It depends on your level of cover and insurance provider.

When you are admitted to hospital, you may have to pay a hospital excess, which is a fixed upfront cost. This number greatly depends on your individual circumstances. You can reduce your excess by paying higher premiums, or reduce your premiums by paying a higher excess.

When it comes to extras cover, it usually only covers part of the cost of services. This can mean a percentage for each service or a certain amount you can claim per year for the same service.

How do Medicare and private health insurance affect your taxes?

It’s important to understand the full cost that goes into receiving Medicare vs private health insurance, because it goes beyond paying upfront fees, gap fees, premiums and excess. So let’s take a look.

Medicare levy

Medicare is funded through the Medicare Levy and Medicare Levy Surcharge. The Medicare levy is 2% of your taxable income, which is calculated at your tax return. Depending on your income, it may be reduced or removed. Often, the tax withheld from your employer includes some funds for the levy.

Medicare levy surcharge

The Medicare Levy Surcharge is a separate and extra levy paid by those who do not have an appropriate level of private health insurance and earn above a certain level of income.

An appropriate level of health insurance means:

- Singles: excess of $750 or less

- Couples/Families: excess of $1,500 or less

For 2025-26, the income threshold rates are:

| Tier | Insurance type | Lower threshold | Upper threshold |

| Tier 1 | Single | $101,0001 | $118,000 |

| Family | $202,001 | $236,000 | |

| Tier 2 | Single | $118,001 | $158,000 |

| Family | $236,001 | $316,000 | |

| Tier 3 | Single | $158,001 | N/A |

| Family | $316,001 | N/A |

This means that if you are a high income earner, you can reduce your tax by avoiding the Medicare Levy Surcharge.

You’ll notice that these rules and incentives are in place to encourage people to get private health insurance and lighten the pressure on the public health system.

How do I avoid the 2% Medicare Levy?

There are a few specific situations where you can avoid or reduce your Medicare Levy. Below are the thresholds for Medicare Levy reductions.

| Does not have to pay (income $) | Qualifies for reduction (income $) | Threshold increase per dependent | |

| Single | $27,222 or lower | $27,222.01 – $34,027 | N/A |

| Single (SAPTO) | $43,020 or lower | $43,020.01 – $53,775 | N/A |

| Family | $45,907 or lower | $45,907.01 – $57,383 | $4,216 |

| Family (SAPTO) | $59,886 or lower | $59,886.01 – $74,857 | $5,270 |

*SAPTO is the seniors and pensions tax offset

You can also get an exemption for the Medicare Levy for a range of reasons that have specific requirements, including:

- Medical exemption

- Foreign resident for tax purposes

- Not entitled to Medicare benefits

- Maintaining a dependent

What is the difference between Medicare and private health insurance?

Medicare is paid for by your taxes and covers treatment and medicine offered in the public health system. Australian citizens and residents are entitled to Medicare. On the other hand, private health insurance is optional, and you have to pay for it yourself to be treated in the private healthcare system.

Other key differences include:

- How much you have to pay out-of-pocket

- The waiting periods for treatment

- Where and which doctor/hospital you get treated at

- What you pay in tax each year

How you pay for healthcare can vary. Depending on your level of cover and the type of treatment, costs may be covered by Medicare, private health insurance, or shared between both—with some out-of-pocket expenses. Make sure to check before your appointment or treatment how it will be paid for.

Medicare vs private health insurance: pros & cons

While private health insurance has many benefits, it can be pricey! So, you do need to weigh up the pros and cons. To help you compare private and public healthcare, we’ve summarised the main pros and cons of Medicare vs private health insurance.

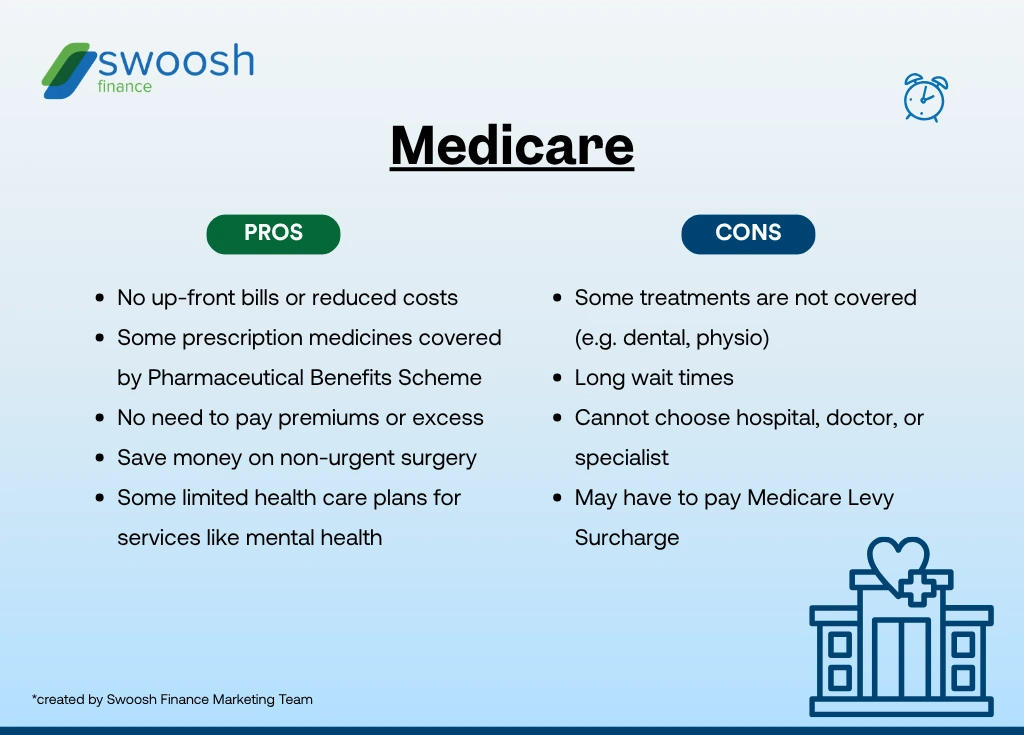

Here, we’ve made a visual summary of the pros and cons of Medicare:

Main advantages of Medicare in Australia:

- Treatment at no upfront cost (or a reduced cost)

- No insurance premiums or excess

Main disadvantages of Medicare in Australia:

- Some treatments aren’t covered

- Longer wait times and less choice

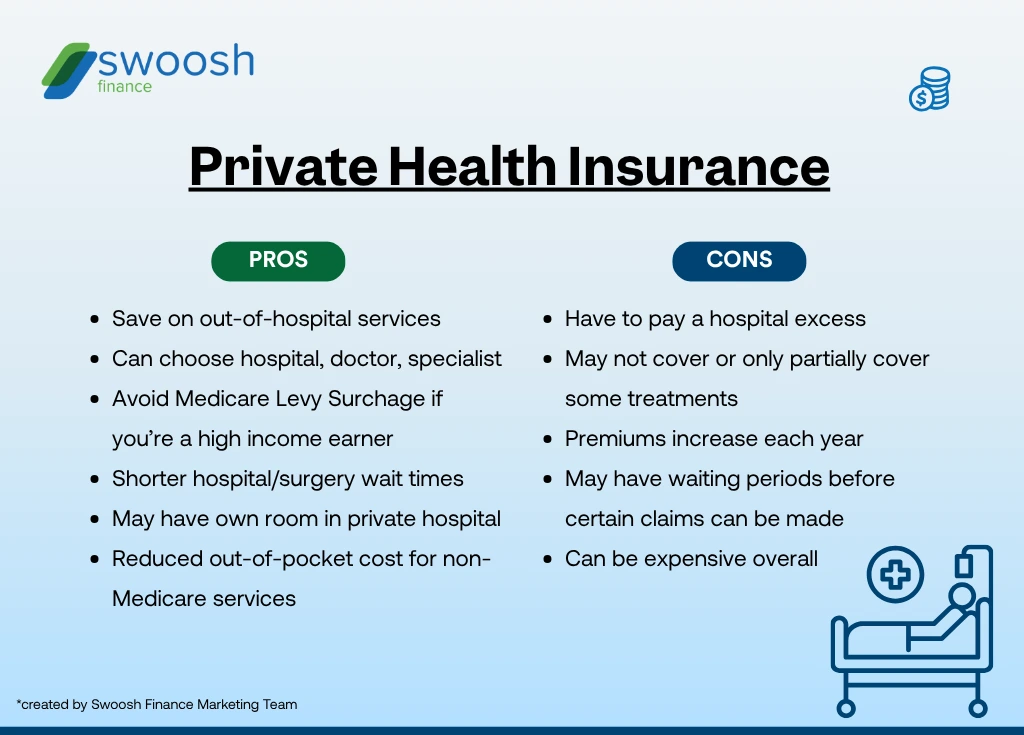

Here is a visual summary of the pros and cons of private health insurance:

Main advantages of private health insurance in Australia:

- Shorter wait times and more choice

- Money saved on out-of-hospital services

Main disadvantages of private health insurance in Australia:

- Must pay an excess when you claim

- Some treatments may not be covered depending on your policy

- Can be expensive

Do you need Medicare if you have private health insurance?

Yes, Medicare is a national insurance scheme and is needed to access public health services. It covers things like emergency services and GP consultations, which private health insurance does not. You can have a combination of both Medicare and private health insurance to cover your bases.

Is Medicare or private insurance better?

Rather than the question being “Medicare vs private health insurance, which is better?”, it’s more about whether private health insurance is worth it for you on top of Medicare.

How? It’s a simple cost-benefit analysis. If you are generally in good health, then your savings may be more valuable elsewhere. You could instead put aside the money you would spend on a premium for emergency expenses—or trust the public system to take care of you. When private health insurance is worth it may depend on your individual situation, like if you have regular medical expenses or a chronic health problem.

If you are looking for an easy way to compare plans, comparison sites like Compare the Market can be a good place to start. They compare dozens of companies at different levels of cover. But be aware, they don’t necessarily have everything listed.

Need a little extra to get you through?

If you need a bit of a boost with your next medical bill, an emergency loan could help you out. Swoosh offers loans with a fast approval process — and it’s all online. Get some help in a pinch by applying in just a few easy steps!

Medicare vs private health insurance FAQs

What is the most popular health insurance in Australia?

Medibank (& AHM) and Bupa are overwhelmingly the most popular health insurance providers in Australia, taking up a combined 52% of the market share. Following behind are HCF, nib and HBF.

What happens if you don’t have private health insurance after 30?

If you don’t take out private health insurance until the 1st July (EOFY) following your 31st birthday, you will have to pay a 2% Lifetime Health Cover loading for each year you are aged over 30 (from when you take out hospital cover).

Can you get a discount on health insurance?

Some insurers may offer age-based discounts for under-30s. You may also be eligible for a government rebate on private health insurance, based on your age and income, which can be applied as a premium reduction or claimed at tax time.