Can a personal loan improve your credit score? It’s a common question, but the answer isn’t quite as straightforward as a simple yes or no. While a personal loan may contribute to your credit history, there’s no magic loan that instantly boosts your score. A range of factors can influence your credit score, and understanding how they work can help you make more informed financial decisions. In this guide, we’ll unpack how credit scores work in Australia, whether a personal loan could play a role, and some practical steps you can take to build a healthier financial future.

Overview:

- Does a personal loan improve your credit score?

- How is your credit score determined?

- How to improve your credit score

- What if you have no credit history?

- When might a personal loan be worth considering?

- Alternatives to taking out a personal loan

- FAQs

Does a personal loan improve your credit score?

A personal loan can affect your credit score, but it won’t automatically improve it.

When you apply for a loan, a credit enquiry is usually recorded on your credit report, which may have a small impact on your score. From there, the effect a personal loan has on your credit profile largely comes down to how you manage it.

Making your repayments on time and staying on top of your debt may help build a positive credit history over time. On the flip side, missed repayments and financial difficulties can have a negative impact.

For people with little or no credit history, a personal loan may also contribute to building a credit profile when it’s managed responsibly. However, everyone’s situation is different, and there’s no guarantee that taking out a loan will improve your credit score.

Below, we’ll look at some of the ways a personal loan can influence your credit score, including how it may help establish a credit history and some common mistakes to avoid.pply. To help you out, we’ll break down how to use a personal loan to increase your credit score and what not to do.

How is your credit score determined?

Before we dive down into getting a personal loan to build credit, it’s good to get an idea of what your credit report and score are made up of. That way you can understand where a small personal loan could help your score improve. As well as how it might negatively impact your score if you don’t manage your debt right.

There are 2 major credit reporting bureaus in Australia. Both calculate your credit score slightly differently. Still, the basic elements involved in calculating your credit score remain the same.

Your score is calculated through the information included on your credit report, including your:

- Repayment history

- Credit applications

- Credit report requests – also called ‘hard’ inquiries

- Defaults

- Credit accounts and products – like credit cards or personal loans

- Repayment history

- Bankruptcy

- Defaults

- Age/length of credit

When you research credit score information be sure to check that it is from Australia. There is a lot of advice for American credit scores out there and it isn’t always relevant to us Aussies.

What doesn’t impact your credit score?

There are plenty of myths about what affects your credit score. While every credit reporting body uses its own scoring model, some factors generally do not directly impact your credit score in Australia.

These include:

- Age: your biological age doesn’t affect your credit score. However, the length of your credit history can matter, as older accounts may help demonstrate a longer track record of managing credit.

- Income: earning a higher salary won’t automatically improve your credit score. Lenders may consider your income when assessing a loan application, but it’s not a direct credit score factor.

- Employment history: changing jobs, working casually, or being self-employed won’t directly affect your credit score, although lenders may review your employment details when deciding whether to approve a loan.

- Your savings balance: the amount of money in your bank account isn’t typically included in credit score calculations.

- Checking your own credit report: reviewing your credit report is considered a soft enquiry and won’t lower your credit score.

- Your gender, marital status or background: personal characteristics such as these are not used to calculate Australian credit scores.

Keep in mind that lenders look at more than just your credit score when assessing an application. Factors such as your income, expenses, employment situation and existing debts can all influence a lender’s decision, even though they may not directly affect your score.

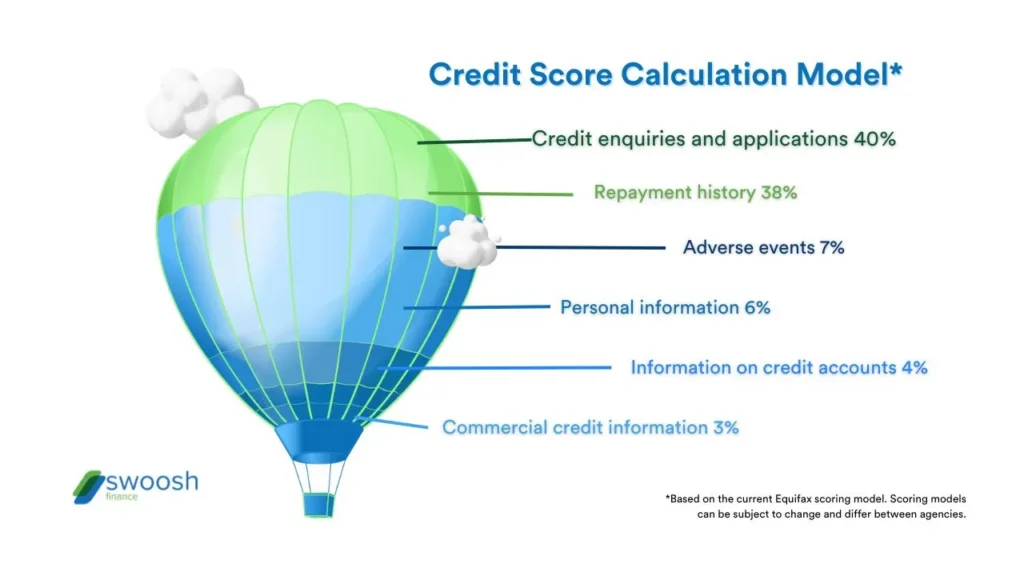

Example of how a credit score is calculated in Australia

Different elements of your credit report are weighted differently when it comes to calculating your rating. Below is a basic breakdown of a standard Equifax scoring model to give you an idea of how the assessment works.

Keep in mind that scoring models and algorithms can change. Also, be aware that this is not a full list of what is included or how much it will affect your score.

Example credit score calculation model breakdown*:

- Credit enquiries and applications 40%

- Repayment history 38%

- Adverse events 7%

- Personal information 6%

- Information on credit accounts 4%

- Commercial credit information 3%

*Based on the current Equifax scoring model. Scoring models can be subject to change and differ between agencies.

Where to get a free credit report?

Checking your credit report is one of the easiest ways to understand your credit health and spot any incorrect information that could affect future loan applications.

In Australia, you’re entitled to a free copy of your credit report from each credit reporting body every 3 months. You can request your report directly from the major credit bureaus below:

Before applying for a loan, it’s worth reviewing your credit report to make sure the information is accurate and up to date.

How to improve your credit score

A good credit score can make it easier to access loans, credit cards and other financial products. While it takes time to build, there are several ways to improve your credit score and strengthen your financial position over the long term.

- Check your credit report regularly: make sure all the information is accurate and dispute any errors that could be affecting your score.

- Pay your bills on time: this includes utilities, phone, and internet bills. Consistent payments help show lenders you’re financially reliable.

- Keep up with loan and credit card repayments: even one missed payment can impact your credit history.

- Limit new credit applications: applying for multiple loans, credit cards or buy-now-pay-later accounts in a short period can lower your score.

- Reduce existing debt: consider paying down high-interest balances and lowering unused credit card limits where appropriate.

- Build an emergency savings buffer: emergency savings may help to cover unexpected expenses and reduce the need to rely on credit.

Remember, improving your credit score doesn’t happen overnight, but small, consistent actions can make a big difference over time.

What if you have no credit history?

Having little or no credit history is not necessarily a bad thing. Unlike some countries where a lack of credit history can make it difficult to access financial products, Australian lenders typically consider a range of factors when assessing a loan application, including:

- Income and employment situation

- Regular living expenses

- Any existing debts or financial commitments

- Your overall ability to comfortably repay the loan

If you have never used credit before, it may simply mean there is less information available about your past borrowing behaviour. However, this does not automatically prevent you from being approved for credit.

It’s important to only apply for a personal loan if you have a genuine borrowing need and are confident you can comfortably afford the repayments. Taking out a loan solely to try to build a credit history or improve your credit score may not be appropriate for everyone.

If you’re unsure about your financial position or whether a loan is right for you, consider seeking independent financial advice before making a decision.

When might a personal loan be worth considering?

While a personal loan isn’t a guaranteed way to improve your credit score, there are situations where it may be a suitable financial tool, depending on your circumstances.

Debt consolidation

If you have multiple existing debts, a debt consolidation loan may help simplify your finances by combining those debts into a single repayment. Before consolidating debt, compare the interest rates, fees, loan term and overall cost to ensure the new arrangement is appropriate for your circumstances.

Building a positive repayment history

Where a lender reports repayment information to a credit reporting body, consistently making repayments on time may contribute positively to your credit history over time. However, there is no guarantee that taking out a personal loan will improve your credit score.

Before applying for any loan, consider whether you need the credit, whether you can comfortably afford the repayments, and whether the product is suitable for your financial circumstances.

Alternatives to taking out a personal loan

A personal loan can be a useful financial tool in the right circumstances, but it isn’t the only option available. Depending on your situation, there may be other ways to improve your financial position, manage existing debts, or cover unexpected expenses without taking on additional credit.

Financial hardship arrangements

If you’re experiencing temporary financial difficulty, don’t suffer in silence. Many lenders, utility providers, and other creditors offer hardship assistance that may help make things more manageable. Depending on your circumstances, this could include adjusted repayment plans, payment pauses, or other support measures.

Negotiating with existing creditors

Before applying for a new loan, it may be worth reaching out to your existing creditors. In some cases, they may be willing to work with you on alternative repayment arrangements that better suit your current situation.

Reducing existing debt

Rather than taking on additional credit, some people choose to focus on paying down their existing debts. Strategies such as prioritising higher-interest balances first may help reduce the overall cost of borrowing and improve your financial position over time.

Financial counselling

Sometimes a little expert guidance can go a long way. A financial counsellor can help you understand your options, negotiate with creditors, and develop a plan to get your finances back on track. Free financial counselling services are available through a range of Australian organisations.

Building an emergency fund

Life has a habit of throwing unexpected expenses our way. Even small, regular savings can help create a financial buffer for future surprises and reduce your reliance on credit when unexpected costs pop up. Exploring practical money-saving tips and finding ways to reduce everyday expenses may help you free up extra cash that can be put towards an emergency fund and other financial goals.

Boosting your income

Improving your financial position isn’t always about cutting back. In some cases, finding ways to earn a little extra income can help ease financial pressure, build savings, or accelerate debt repayments. Whether it’s picking up extra shifts, freelancing, selling unused items, or exploring legitimate ways to make money online, even a small increase in income can make a meaningful difference over time.

Reviewing recurring expenses

Subscriptions, memberships, and other recurring expenses can quietly add up over time. Reviewing your regular spending is one of the most effective money-saving habits, helping free up extra cash for savings goals, debt repayments, or other financial priorities.

Government and community support services

Depending on your circumstances, you may be eligible for government assistance or support from community organisations that can help ease financial pressure and connect you with additional resources. We’ve compiled a handy list of Australian organisations in the table below:

| Service | What they offer |

| National Debt Helpline | Free information, resources, and access to financial counsellors who can help you better understand your options. |

| Australian Competition and Consumer Commission (ACCC) | Information about consumer rights, debt collection practices, and managing financial obligations. |

| Australian Financial Security Authority (AFSA) | Guidance and resources to help Australians understand their options when dealing with debt. |

| Services Australia – Dealing with Debt | Practical information about budgeting, managing debt, and accessing available support services. |

| MoneySmart – Financial Counselling | Information about financial counselling and other tools that may help you manage your finances. |

| Way Forward | A not-for-profit organisation that helps eligible Australians explore solutions for managing unsecured debt. |

Looking for a lender that sees more than your credit score?

At Swoosh Finance, we know your credit score is only part of the picture. We take a balanced approach to assessing applications and look at more than just the numbers. With straightforward eligibility criteria, responsible lending practices, and a simple online application process, our bad credit loans could help you access the funds you need. Apply online today!

FAQs

What is a good credit score?

There isn’t one universal credit score in Australia, as different credit reporting bodies use different scoring ranges. Generally speaking, a higher score indicates a lower credit risk, but lenders look at more than just your credit score when assessing an application.

How to check my credit score?

You can request a copy of your credit report from a credit reporting body such as Equifax or Experian. Many providers also offer free access to your credit score online.

Does Afterpay affect credit score?

Usually, no. Using Afterpay won’t affect your credit score. However, missed payments may result in fees, account restrictions, or other consequences that could impact your credit profile in some situations.

Does paying off a loan improve your credit score?

Paying off a loan doesn’t automatically improve your credit score. However, consistently making repayments on time throughout the life of the loan may contribute positively to your credit history where repayment information is reported to a credit reporting body.